It was the best of times, it was the worst of times, it was the age of wisdom, it was the age of foolishness, it was the epoch of belief, it was the epoch of incredulity, it was the season of Light, it was the season of Darkness, it was the spring of hope, it was the winter of despair, we had everything before us, we had nothing before us, we were all going direct to heaven, we were all going direct the other way – in short, the period was so far like the present period, that some of its noisiest authorities insisted on its being received, for good or for evil, in the superlative degree of comparison only.

― Charles Dickens, A Tale of Two Cities

The High Cost of Doing Business

Despite enormous revenues generated by the pharmaceutical industry and its status as one of the most lucrative investment sectors for large-scale investors, the pharmaceutical industry has been facing a looming set of crises that threaten its ability to continue generating meaningful rates of returns for investors.

Big Pharma’s decaying business model has been an open secret for nearly two decades, causing grave concern among industry insiders and financial analysts.

As far back as 2003 global consulting firm Bain & Company warned, “The blockbuster business model that underpinned Big Pharma’s success is now irreparably broken.”

Blockbuster drugs, which are defined as products with total annual sales of over $1 billion, have historically provided the financial basis for most research-based pharmaceutical companies to sustain their innovation- driven research and development (R&D) models. But analyses indicate that pharmaceutical companies are increasingly struggling to deliver these golden eggs, suggesting that the traditional blockbuster model is broken.

Bain’s 2003 report, “Rebuilding Big Pharma’s Business Model,” highlighted pharma’s declining rates of return:

Declining R&D productivity, rising costs of commercialization, increasing payor influence and shorter exclusivity periods have driven up the average cost per successful launch to $1.7 billion and reduced average expected returns on new investment to the unsustainable level of 5%. [Emphasis added.]

The report’s conclusion was unequivocal and stark. “Pharmaceutical companies need new business models to restore healthy financial results,” wrote Bain. [Emphasis added.]

Big Pharma responded by disregarding Bain’s warnings, kicking the can down the road, and soldiering on with the rotting corpse of their antiquated business model of investing more resources into R&D development.

Fourteen years after the Bain report, one of largest professional services networks in the world, Deloitte Touche Tohmatsu Limited, headquartered in London, issued a stark warning in its annual report, “Measuring the Return from Pharmaceutical Innovation: A New Future for R&D?,” in which it cited an enormous decline in projected R&D returns for the dozen largest pharma companies.

In the same report, Deloitte assessed a decline in combined R&D returns for this cohort of companies from 10.1% in 2010 to a mere 3.2% in 2017.

The Deloitte report highlighted the acute market pressures pharma faced as development costs continued to escalate. In 2010 the cost to bring a new product to market for this cohort was $1.188 billion. By 2017 these costs had risen to a record $1.992 billion. And by 2022 development costs had hit $2 billion.

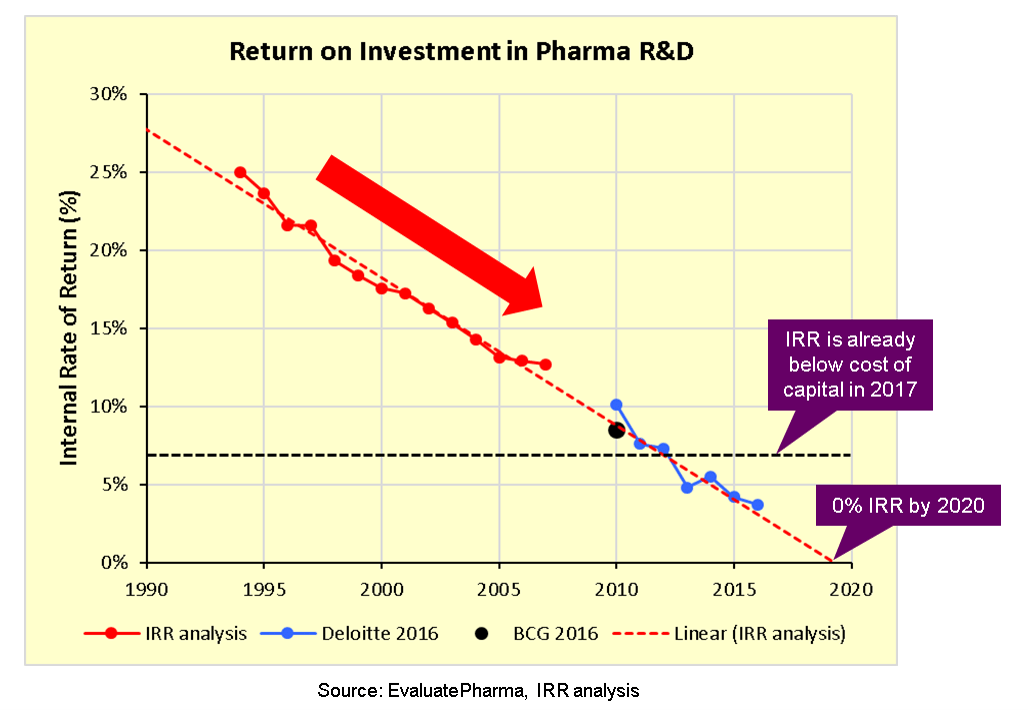

In 2017, pharma analyst Kelvin Stott wrote a piece, “Pharma’s broken business model: An industry on the brink of terminal decline.” His graphic illustration, in a single chart, of the grim realities of what pharma is facing received widespread attention among industry analysts.

With a big red arrow pointing down a steep trajectory, Stott graphically illustrated how pharma’s Internal Rate of Return (IRR) had sunk below the cost of capital in 2017 and would sink to 0% by 2020 at its then-current rate of decline.

Stott made the point that incremental improvements in productivity would not solve this crisis:

[I]mproving R&D productivity by 5% or even 10% each year from 2018 would slow, but not reverse[,] the current decline in nominal ROI and IRR. [. . .] We would need to increase nominal R&D productivity/ROI by at least 20% each year to reverse the projected decline in P&L performance, and even then, the industry’s sales and profits would fall by about one third before they begin to pick up again in 2030.

Of the many aspects of pharma R&D, few are as time-consuming, precarious, and costly as a new drug’s Phase III clinical trials—the last phase of testing before results are submitted to the regulatory authorities for licensure, which allows for the drug’s release to market. Phase III trials are required to complete multi-year safety testing in human subjects and are intended to serve as a comprehensive check for adverse effects of a new product.

In a 2012 report, “STIFLING NEW CURES: The True Cost of Lengthy Clinical Drug Trials,” the Manhattan Policy Research Institute (MPRI) detailed the nettlesome realities that these trials can present to an industry seeking to maximize profit at all costs.

Asserting that the current system for drug approval “discourages innovation and investment” and that “the main culprit” hindering innovation is the high cost of Phase III clinical trials, MPRI recommended, “If the United States adopted a flexible, conditional approval approach that allowed sponsors to recoup some of their R&D costs before, or during, large-scale clinical trials,” it could lower the costs of drug development.

In its conclusion, MPRI suggested that legislative action was needed to alter the current regulatory processes:

Congress, therefore, should create clear standards for conditional approvals and also give the FDA more flexibility to develop new regulatory tools that are better adapted to the rapid advances in basic science and that have the potential to accelerate patient access to safer and more effective therapies. [Emphasis added.]

The MPRI report echoed the figures presented by Deloitte. It noted that the average amount spent on R&D for a drug approved by the US Food and Drug Administration (FDA) was $100 million in 1975 and $1.3 billion in 2005—a more than tenfold increase in 30 years.

The MPRI report went on to state:

The biggest driver of this phenomenal increase has been the regulatory process governing Phase III clinical trials of new pharmaceuticals on human volunteers. Phase III clinical trials have become far larger and more complex than they were in the past. From 1999 to 2005 the average length of a clinical trial increased by 70 percent; the average number of routine procedures per trial increased by 65 percent; and the average clinical trial staff work burden increased by 67 percent.

The combined impact of these factors has resulted in Phase III trials totaling around 40% of R&D expenditures.

But the enormous impact of the “sunk costs” associated with Phase III trials on Big Pharma is even more profound than this percentage of R&D costs indicates. The reason is that many of the drugs that enter the Phase III trials end up being unsuccessful and are dropped. As a result, their steep costs never translate into eventual profits. When we look at only the drugs that do make it through the trials and do get approved, we see that Phase III trials represent a whopping 90% or so of the development costs of a single drug that goes the distance from laboratory to market.

Certainly, pharmaceutical companies would welcome any mechanism or legislative action that would allow them to circumvent lengthy regulatory processes and shortcut costly clinical trials and safety requirements.

Likewise, sidestepping any requirements that might hinder rapid commercialization of new drugs would optimize the substantial capital investments involved in bringing drugs to market while reducing sunk costs.

In short, anything that would allow pharma to cut corners would represent a significant windfall and increase the appeal of the industry in the eyes of investors.

Falling Off the Patent Cliff

Paralleling the industry’s problem of skyrocketing R&D costs is the imminent “patent cliff” for a significant number of Big Pharma’s high-profile drugs. Together, these impediments to free-wheeling profiteering, along with massive advertising expenditures, have created a perfect storm for the Pharma Cartel and its investor class, who have little tolerance for declining rates of return and risky investments.

The term patent cliff describes how a product’s revenues and profitability “fall off a cliff” once the exclusive rights granted by patent protection expire. After a product goes off-patent, generic competitors are allowed to manufacture and sell that product at much lower prices.

Lately, “patent cliff” has come to be associated almost exclusively with the pharmaceutical industry. It underscores the gravity of patent protection to pharmaceutical firms.

In her 2022 article “Looming Patent Cliff will be Pharma’s Moment of Truth” Gail Dutton put a fine point on the seriousness of the issue when she attached figures to the coming revenue loss:

$236 billion in pharmaceutical sales [are] at risk between now and 2030. For context, the top 10 biopharmas in 2021 had total, global sales of approximately $512 billion. In the next eight years, more than 190 drugs will go off-patent for these companies. Of those, 69 are blockbuster drugs.

Dutton’s quote of Maria Whitman, global head of ZS Associates’ pharmaceutical and biotech practice, corroborated the magnitude of the situation:

Depending on the company, on paper, the losses represent from 14% to 79% of their revenues. That’s $6 [billion] to $38 billion that any one company will lose in revenues. Another way to think about it is, 5 of today’s top 10 pharmas (by income) will have more than 50% of their revenues at risk. [Emphasis added.]

Piling on with a March 2023 piece, “The BioPharma Patent Cliff: 2023 and Beyond,” intellectual property attorney Jason Mock further confirmed that “several top drugs are set to lose U.S. exclusivity as patents expire or settlements allow for generic entry.”

Mock explained that the tipping point for Big Pharma is no longer in the distance:

Between now and 2030, the biopharma sector is expected to be rocked by a number of high-profile patent cliffs that are likely to reshape the market in potentially unpredictable ways. For example, many estimates suggest that the largest biopharma companies—such as Bristol Myers Squibb, Pfizer, and Amgen—will see significant percentages of their revenues absorbed by competitors launching copycat products. [Emphasis added.]

The message being sent to Big Pharma from industry analysts and investors is clear: Continuing to kick the can of the blockbuster business model down the road is no longer an option. The hunt for exploitable new molecules to be “cured” by phenomenally profitable blockbuster drugs has reached the end of its financial lifeline. A new commercial and organizational model will have to be invented if Big Pharma wishes to keep up with the demands of large-scale investors.

Desperately Seeking Solutions

It is impossible to overstate the value that large pharmaceutical and medical industries bring to investment management megafirms like BlackRock Inc., The Vanguard Group, Inc., and State Street Corp. Indeed, pharmaceuticals and the entire “health management system” represent one of the largest sectors of the US economy. Thus, a threat to the operations and profitability of the pharmaceutical industry poses a threat to those enormous financial interests. The overlords of the investment behemoths go to great lengths to protect and further their interests and their power—and those of the clients whose vast sums of money they manage.

In the past, Big Pharma has been able to offset or delay financial deterioration by continuing to develop products in the pipeline and capitalize on those products as they came online.

Circa 2023, the days of singlehandedly placing big bets on a few molecules, marketing them heavily, and turning them into massive money spinners, are over. The business model the pharma leviathan has relied upon for decades to generate enormous revenue is irreparably broken.

As former chief executive of GlaxoSmithKline J.P. Garnier pointed out, Big Pharma’s once-reliable meal ticket has become “a business model where you are guaranteed to lose your entire book of business every 10 to 12 years.”

While financial analysts and industry journalists speak openly about this existential dilemma, pharma CEOs, corporate board members and health bureaucrats, with the help of governmental agencies, have been aggressively pursuing “novel” solutions and setting in motion strategies to restructure existing systems and reorient the pharma juggernaut.

These strategies and solutions are designed to “blow up” the obsolete structures of the old pharma business model in order to create space for profitable replacements. “Revolutionary” innovations, alternative regulatory procedures, and new markets promise a seismic shift in how Big Pharma operates.

A Brave New World of biopharmaceuticals, public-private partnerships, regulatory reform, strategic initiatives, and all manner of “creative disruptions” are knocking at the door.

Buyer beware.

In Part 2, we will look at where the Big Pharma colossus is heading, at the details of the industry’s “revolutionary innovations” and at the various mechanisms involved in bringing about a radically revamped pharma program.

{kind=link}